Asia Cement's Below-Cash Delisting Offer: It’s a Bad Deal for Minority Shareholders

Asia Cement (SEHK:743) has received a privatization offer from its major shareholder at HK$3.22 per share. While this price represents a nearly 30% increase over the previous closing price of HK$2.53, we believe the offer is unreasonably low. It seems the offeror is taking advantage of the ongoing downturn in both the cement and real estate markets in China to privatize the company at a favorable price, a move that disadvantages minority shareholders.

Our assessment, based on financial calculations, indicates that the offer price is less than the company’s net cash value per share:

Cash and cash equivalents = ¥9,256,549

Total liabilities = ¥3,076,098

Non-controlling interest = ¥363,950

Net cash = ¥5,816,501

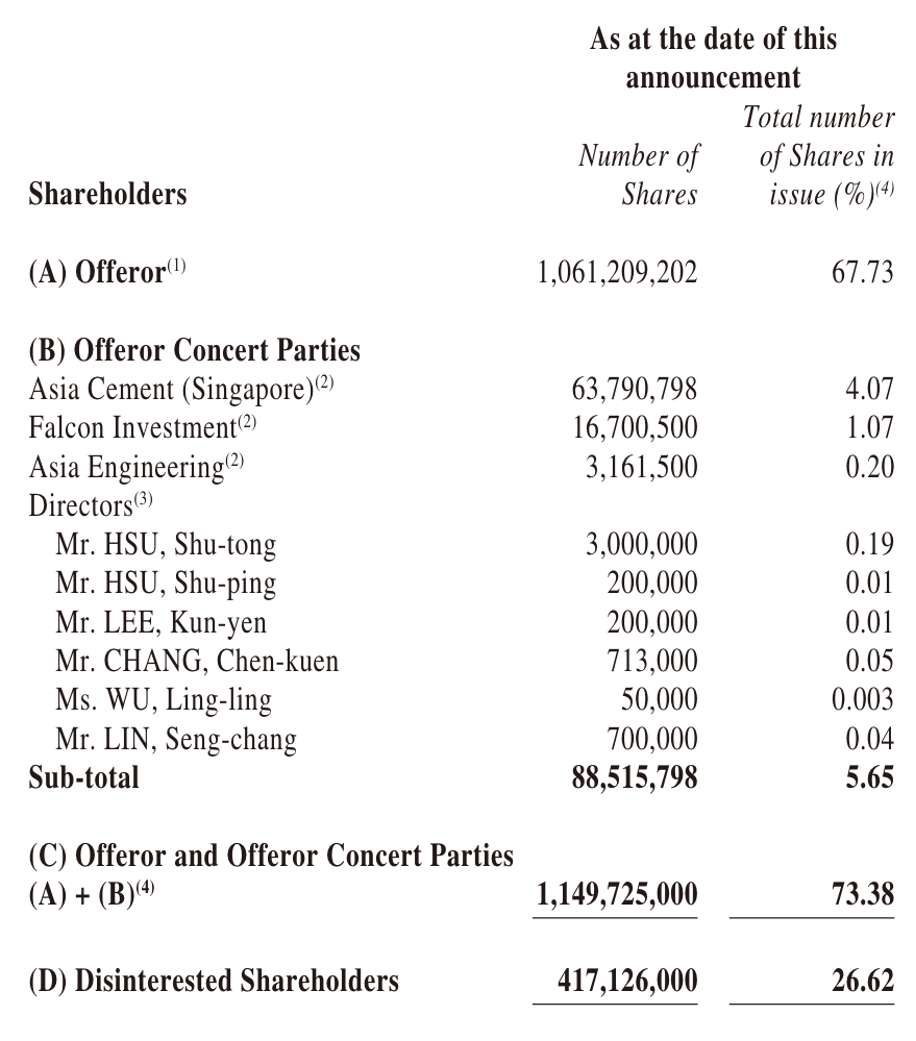

Number of shares = 1,566,851

Net cash per share = ¥3.71

Net cash per share in HKD = HK$4.01

With the offer priced at HK$3.22, it translates to a 20% discount to the net cash per share. Effectively, the offeror is able to buy the company at HK$0.80 less per share than the cash value per share, essentially getting HK$1 back for each HK$0.80 spent.

This analysis clearly shows that the offer undervalues Asia Cement, making it an unfair proposal for the shareholders.

Analyzing the stock chart of Asia Cement, the company enjoyed a robust rally from 2017 until the onset of the Covid-19 pandemic. Since then, the share price has been on a downward trajectory. Currently, the stock has reverted to its trading range from 2009 to 2017. This backdrop makes the timing of the offer from the major shareholder appear opportunistic. Given the prolonged period of declining share prices, coupled with a pessimistic outlook on the Chinese property sector and lackluster overall stock market performance, investors may be feeling weary. This context likely makes the current offer seem more appealing than it might otherwise be, suggesting the Offeror is seizing an opportunity to capitalize on investor fatigue.

We are skeptical about the success of the Offer, primarily because it involves a scheme of arrangement that requires shareholder approval through a vote, even despite the Offeror already holds a substantial 73.38% stake in the company.

For the scheme of arrangement to be approved, it requires the consent of 75% of the disinterested shareholders, and no more than 10% should oppose it. In this scenario, the Offeror cannot participate in the vote. Given the unattractiveness of the low offer, it's unlikely to garner enough support from shareholders.

This sentiment is reflected in the stock's price action following the announcement: Asia Cement’s share price dropped to HK$2.84, falling below the offer price. This suggests that the market also doubts the deal will succeed.

However, this situation could be a strategic move by the Offeror to acquire more shares through this opportunity. By making the offer, the Offeror might attract more sellers in a stock that typically sees low liquidity.

According to the announcements, UBS has been purchasing shares on behalf of the Offeror. Here is a screenshot example:

The Offeror's ability to acquire shares below the offered price suggests a possibility of increasing their stake beyond 75%. Should this occur, Asia Cement might breach the Hong Kong Stock Exchange’s minimum free float requirement of 25%, potentially leading to a trading suspension. Subsequently, another offer could be made after the first one fails. In such a scenario, the suspension might compel more shareholders to accept an undervalued offer, potentially facilitating the eventual delisting of Asia Cement. This is speculative and not a definitive outcome.

We believe enlightened shareholders of Asia Cement would reject such an undervalued offer, and even more so, avoid selling their shares in the open market below the offer price.

Disclosure and Disclaimer: We do not own shares in Asia Cement, and we are not licensed financial advisors.