Growth Dragons Weekly: China Stocks Gained This Week After Government Intervention

In Growth Dragons this week:

China Stocks Gained This Week After Government Intervention

Lower Mortgage Rates And Down Payments For First Property Purchase In China + Impact To Banks

China’s Largest Real Estate Agency Reports 41% Revenue Growth In 2Q23 + Share Price Gained 27%

Home Appliances Demand Continue To Rise

PDD’s Solid Results And Temu Expands To Southeast Asia + PDD Shares Gained 27%

1. China Stocks Gained This Week After Government Intervention

This week, the Chinese government made three moves aimed at supporting the stock market:

Reducing Stock Stamp Duty: China has halved the stamp duty on stock trading. The finance ministry announced a reduction in the 0.1% duty on stock trades.

Managing Fund Managers' Trading: Stock exchanges have instructed several major fund houses to refrain from selling more A shares than they purchase for a day.

Expediting Approval of New Funds: China's securities regulator has approved the launch of 37 retail funds in the hope of attracting fresh capital into the market. These funds include 10 exchange-traded funds (ETFs) that track the small-cap CSI 2000 Index and seven tech-focused ETFs. The remaining 20 products are innovative mutual funds that, for the first time, charge investors floating fees based on fund size, performance, or holding period.

However, there is uncertainty about whether these measures can sustain the market. China's stocks have experienced numerous false rallies, and these measures may not have a significant impact. The stamp duty reduction may not address the main reasons why investors are hesitant to invest, as the duty was not particularly high to begin with. Additionally, instructing mutual funds to halt selling temporarily may not be a sustainable policy, as these funds may eventually need to sell due to investor withdrawals.

Nevertheless, the rise in share prices this week is still a welcomed change.

MSCI China saw a 3% increase this week. It's worth noting that this refers to the version listed in the US under the ticker MCHI, as the Hong Kong market was closed due to a typhoon.

Similarly, we opted to use iShares MSCI China A (CNYA) as a substitute for a CSI 300 ETF to track the performance of A shares this week, and it recorded a 2% increase, indicating a rebound in onshore stocks as well.

2. Lower Mortgage Rates And Down Payments For First Property Purchase In China + Impact To Banks

The Chinese Government has made a more significant policy shift with regards to home purchasing. Commencing on September 25, first-time homebuyers with mortgages now have the option to request lower interest rates on their existing loans from their banks.

This reduction in mortgage rates is expected to benefit approximately 40 million borrowers. To illustrate, if the interest rate on a 1-million-yuan ($140,000) mortgage with a 25-year term is lowered from 5.1 percent to 4.3 percent, borrowers would see their annual interest payments decrease by more than 5,000 yuan.

Furthermore, the minimum down payment requirements for first-home and second-home purchases have been lowered to 20 percent and 30 percent, respectively, down from the previous levels of 30 percent and 40 percent.

These policy changes represent significant shifts, and our perspective on them is mixed. On one hand, we believe that China should heed the lessons from the property crisis to avoid perpetuating an excessive fixation on real estate. However, we also hope for a swift recovery of the Chinese economy. It's important to note that these measures primarily target individuals with only one property, which is fair. Nevertheless, the reduction in the down payment ratio for second properties may inadvertently contradict the message that homes are for staying and not for speculation. In any case, it remains to be seen whether these changes will lead to an increase in real estate transactions.

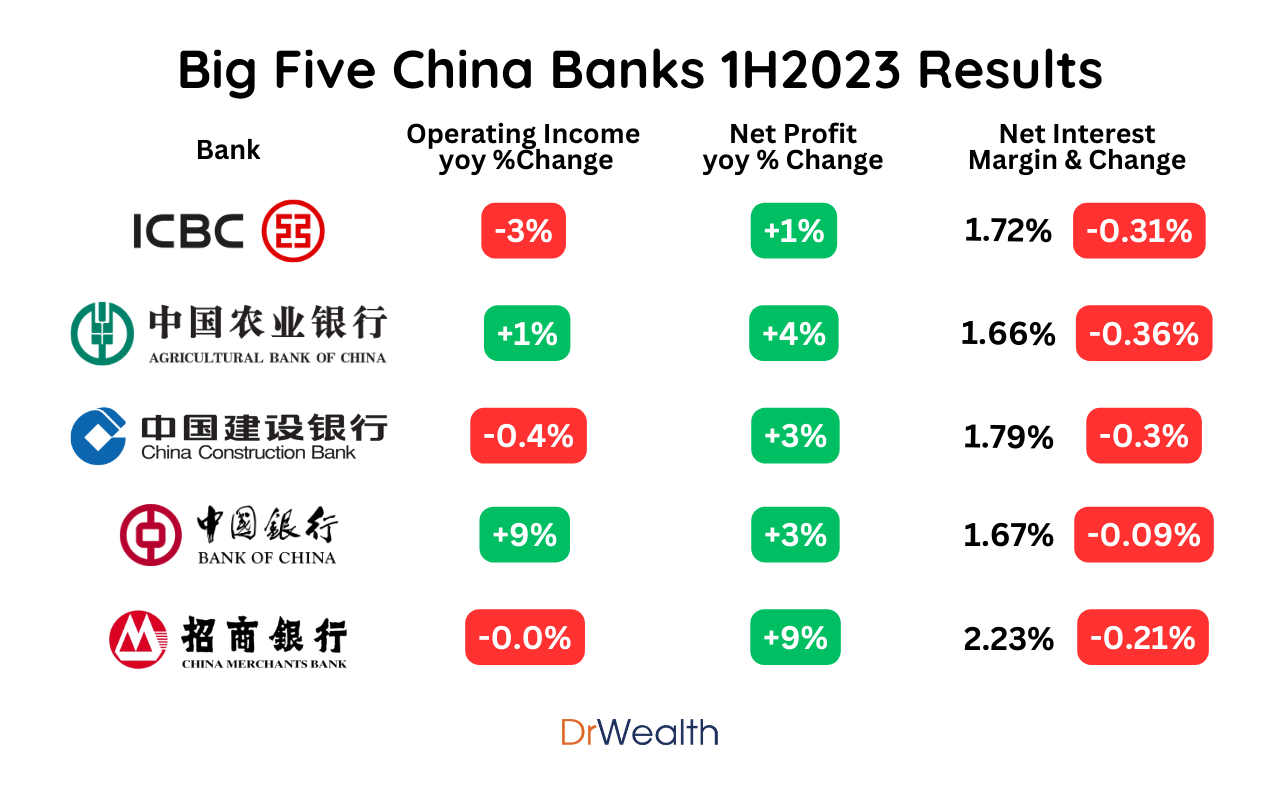

Lowering mortgage rates could also negatively affect banks' income. The five major banks in China have recently released their half-year results, all of which show a decrease in net interest margin. This decline can largely be attributed to China's reduction of the Loan Prime Rate and a lack of demand for loans.

In an effort to mitigate the impact of lower mortgage rates, China's largest banks have also reduced interest rates on deposits by varying amounts, ranging from five to 25 basis points. Nevertheless, it is anticipated that Chinese banks' net interest margins will continue to shrink in the second half of this year.

We believe that the banks should prioritize sacrificing their margins at this juncture in order to stimulate lending and promote economic growth. In the long term, these banks will reap benefits as their loan portfolios expand. Additionally, lower interest rates may help prevent an increase in defaults.