Growth Dragons Weekly - Jun 2023 #4

In Growth Dragons this week:

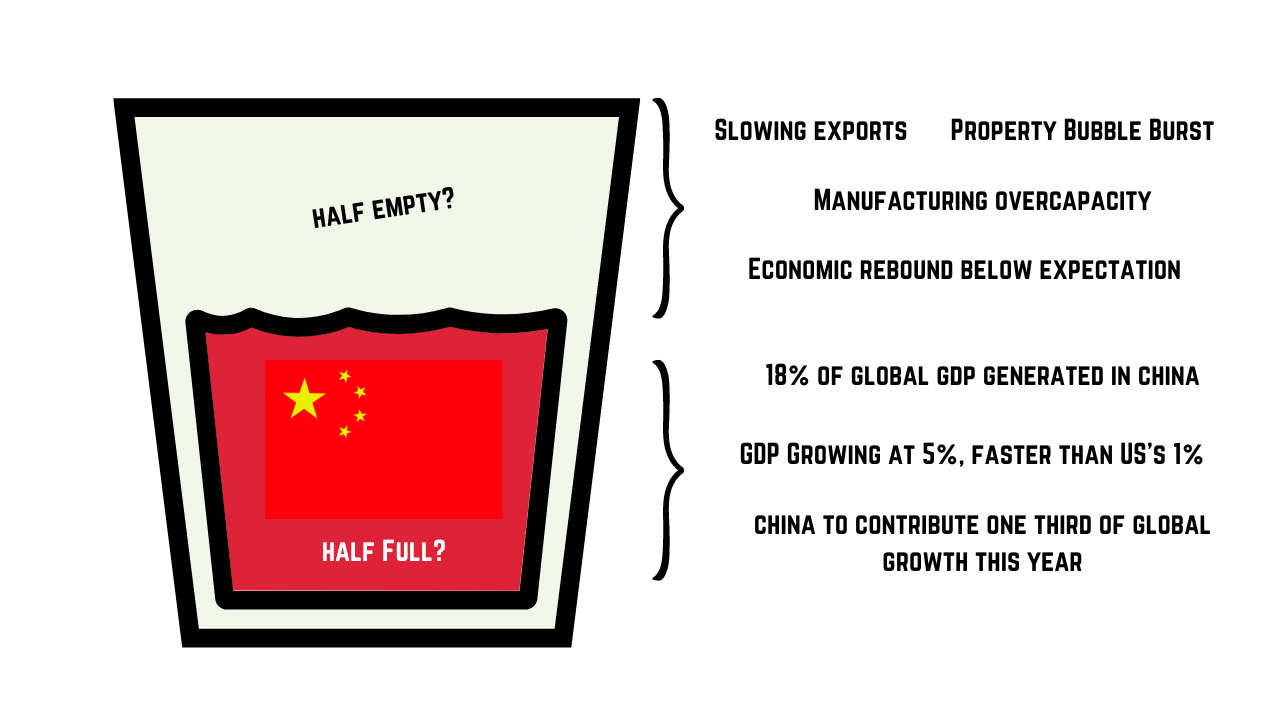

China’s Economy: Half-Cup Empty or Half-Cup Full?

Weakening Yuan, so what?

Deleveraging is in Progress and Makes China Economy More Robust

Lackluster IPOs but Expect Second Half Improvement

China’s Economy: Half-Cup Empty or Half-Cup Full?

China's economic performance remains underwhelming, but we believe the primary issue lies in excessively high expectations and the negative narrative propagated by the Western world, rather than China's actual performance. Despite this, China's GDP is expected to experience a growth of 5% in 2023, surpassing the forecasted growth rate of just over 1% for the US. It is possible that investors were anticipating a 10% growth from China, causing them to perceive the 5% growth as falling short. Moreover, the media has consistently portrayed China's economy as troubled, despite its considerably faster growth compared to the US. Regrettably, objectivity in Western media regarding China seems to be lacking in recent times.

Let's examine the recently released economic data from China.

The manufacturing Purchasing Managers' Index (PMI) for China indicates a continued contraction in June, standing at 49 (a value below 50 indicates contraction). However, the positive aspect is that there was no further deterioration, suggesting a potential sign of a turnaround.

Taking a closer look and delving into the profitability of industrial companies, the recent data from the National Bureau of Statistics reveals a 12.6% year-on-year decrease in profits for May. From January to May, profits experienced an 18.8% decline, which showed a slightly slower rate compared to the nearly 21% drop witnessed in the first four months of 2023.

During the first five months of the year, profits at foreign firms declined by 13.6%, displaying a marginal deceleration compared to the January-to-April period. Additionally, profits at private firms witnessed a substantial decrease of 21.3%, while state-owned enterprises saw a decline of 17.7%.

In May, exports experienced a decline for the first time in three months, while imports continued their downward trend. The exact cause of these developments remains uncertain. It is possible that factors such as derisking and supply chain restructuring have led to reduced demand and manufacturing overcapacity. Another potential factor could be the restriction on the sale of high-end equipment and chips to China, directly impacting imports. The bearish property market may also be contributing to the overall situation, as it no longer provides significant support to the economy. Additionally, domestic consumption might not be meeting expectations, as Chinese individuals are saving more money than ever before. Regardless of the specific reason, it is evident that overcapacity exists and it will take some time for the market to regain equilibrium.

Despite the discouraging figures and prevailing sentiment, Chinese Premier Li Qiang, during his speech at the opening plenary of the World Economic Forum's Annual Meeting of the New Champions a few days ago, expressed confidence that China remains on track to achieve its annual growth target of approximately 5%.

Interestingly, Wall Street analysts are even more optimistic, forecasting growth of over 5% for China in 2023. Although these analysts had previously projected higher figures and subsequently adjusted their estimates, this reflects the initial excessively high expectations surrounding China's growth. When China initially announced a 5% target, many considered it to be a conservative estimate. However, as expectations have fallen short, it appears that China's projections were more aligned with reality.

In contrast, the World Bank has revised its forecast for China's growth this year to 5.6%, up from the previous estimate of 4.3%. Similarly, the International Monetary Fund (IMF) has raised its GDP forecast for China to 5.2%, an increase from the earlier projection of 4.4%.

During a CNBC interview, Joe Ngai, Chairman of McKinsey & Company Greater China, effectively articulated the distinction between two contrasting perspectives. He aptly described how the pessimistic individuals tend to adopt a "glass half-empty" outlook, which unfortunately aligns with the viewpoint adopted by Western media. Here are his comments:

Taking the “glass half-empty” perspective: If you look at all the challenges that China is facing like overcapacity in many sectors, exports being hit by a slowing global economy, and the over-hang of residential real estate, the compression on margins is being felt by every business. For a lot of businesses coming out of COVID-19, the big rebound is just not happening.

Taking the “glass half-full” perspective: 18% of global GDP is generated in China. The economy will grow at least 5% this year, and this represents a third of global growth. There’s no other economy of this size that’s growing at this pace. Many of the macro factors that we love about China are still very much present.