The Prominent 10: China’s Top Growth Stocks According to Goldman Sachs

Goldman Sachs has identified a group of “Prominent 10” large-cap Chinese private-sector companies that it expects to lead the market in the years ahead. Goldman projects they’ll grow earnings at an average of ~13% annually through 2026.

What makes this group stand out is how clearly they align with the structural themes driving China’s next phase of growth:

AI and advanced tech development

Aggressive “Going Global” expansion

New forms of services and domestic consumption

And they’re doing it with policy tailwinds, not headwinds. With Beijing easing off its previous crackdown and pushing new laws to promote private enterprise, these firms are in a stronger position to invest, scale, and expand.

For investors, the opportunity lies in valuation. As a group, the Prominent 10 trade at just a 22% forward P/E premium to the CSI 300—a far cry from the 43% premium investors are paying for the U.S. Magnificent 7. There’s also headroom from a market-weighting perspective: China’s top 10 companies make up just 17% of the market cap, compared to 33% in the U.S. and over 50% in Korea, France, and Germany. In other words, these firms could grow into a much larger share of the index—if they deliver.

Ranked by market cap, here are the Prominent 10—and why they deserve attention:

#1 Tencent (700)

Tencent needs no introduction. As China’s largest internet company, it dominates daily life through its all-in-one WeChat super-app, used by over 1.3 billion people. Virtually everyone in China relies on it for messaging, payments, content, and services—making it a digital infrastructure layer that businesses plug into. This immense user base powers Tencent’s other segments—gaming, fintech, advertising, and cloud—creating a flywheel of engagement and monetisation.

AI Development: Tencent is pouring capital into AI, from training large models to integrating them into WeChat and its cloud services. It’s already using AI to boost ad targeting and automate customer interactions. As Goldman points out, scale matters in AI—and Tencent has the resources to compete at the top.

Going Global: While Tencent remains China-focused, its gaming division is a global force. Through full ownership of Riot Games (League of Legends) and stakes in Epic Games, Supercell, and others, Tencent earns meaningful overseas revenue and brings Chinese-developed titles to global players.

New Consumption Trends: China’s shift toward digital services—be it mobile gaming, streaming, or social commerce—directly benefits Tencent. Time spent online increasingly flows through its platforms, reinforcing its dominance in both consumer attention and monetisation.

Valuation: Tencent trades at about 21× trailing P/E and 17× forward P/E, both below its 5-year average of 22×. Compared to U.S. peers like Meta (24×) or Alphabet (28×), Tencent is undervalued for a business of this scale and embeddedness. If earnings continue to grow—and they are—there’s room for meaningful re-rating.

#2 Alibaba (9988)

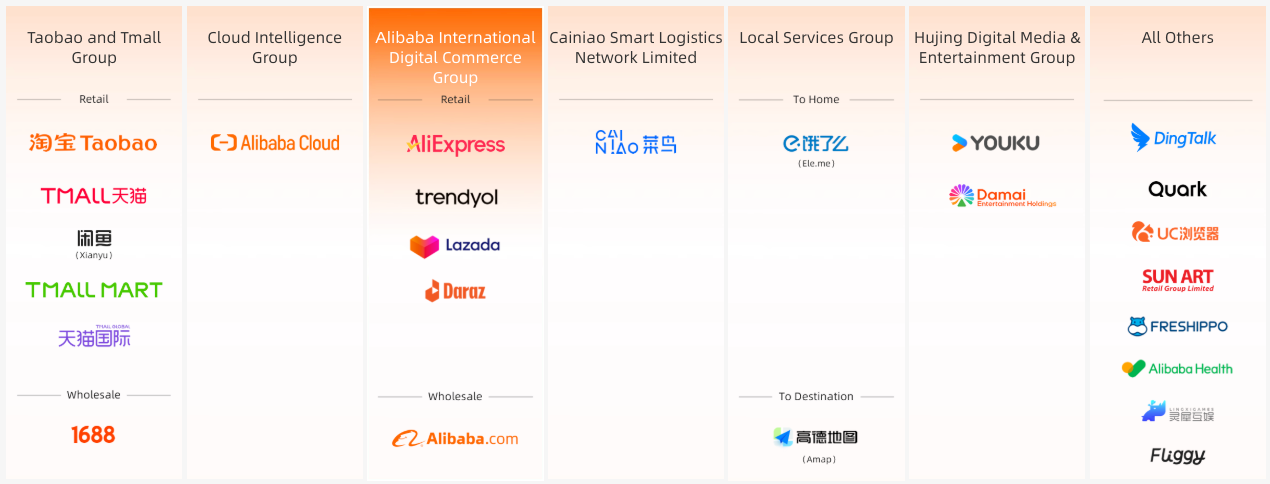

Alibaba is China’s e-commerce heavyweight and a major force in cloud computing. Often seen as China’s equivalent of Amazon + AWS, Alibaba anchors the country's retail infrastructure through its Taobao and Tmall platforms. With hundreds of millions of consumers and millions of merchants, it benefits from powerful network effects that competitors find nearly impossible to replicate. Its integrated logistics (Cainiao) and payments (Alipay) ecosystems deepen its moat. Beyond e-commerce, cloud computing and international commerce are key drivers of future growth.

AI Development: CEO Eddie Wu has called AI one of Alibaba’s most critical strategic priorities. The company has developed its own large language model, Tongyi Qianwen, and is embedding AI across e-commerce and cloud services—from smarter product recommendations to more efficient supply chains. Alibaba Cloud is positioned to power AI infrastructure for enterprises across Asia.

Going Global: Alibaba’s global expansion is gaining traction. Its international commerce segment—including AliExpress, Lazada, and Trendyol—grew 32% year-on-year, showing strong momentum in regions like Southeast Asia and Europe. By connecting Chinese manufacturers directly to overseas buyers, Alibaba is building scale across borders and reducing reliance on the domestic market.

New Consumption Trends: On the home front, Alibaba continues to benefit from China's shift toward digital, mobile-first consumption. Consumers in lower-tier cities are coming online, grocery and food delivery are growing fast, and online entertainment is a rising category. Alibaba is also a major player in “new retail,” blending offline stores with online fulfilment and data-driven operations.

Valuation: After years of regulatory overhang and investor fatigue, Alibaba is trading at a trailing P/E of ~15× and a forward P/E of just ~11×—almost a 50% discount to its 5-year average of 29×. That’s despite double-digit growth in key business units like cloud and international commerce. If sentiment turns and growth accelerates, a significant re-rating is on the cards.

#3 Xiaomi (1810)

Xiaomi is best known for its smartphones, but it’s far more than that—it’s a consumer tech ecosystem spanning smart home devices, wearables, and now electric vehicles. Its strategy of delivering high-spec gadgets at aggressive prices has won it massive market share; it now ranks #3 globally in smartphone volume, behind only Apple and Samsung. Over the years, Xiaomi has built a loyal fan base and a trusted brand across a wide spectrum of consumer electronics.

AI Development: AI is baked into Xiaomi’s product philosophy. Its phones feature AI-powered photography and personalization, while its HyperOS operating system links smartphones to smart TVs, air purifiers, and even EVs. Xiaomi is also building autonomous driving capabilities for its upcoming electric car, and has developed its own voice assistant. As an IoT leader, Xiaomi is well-positioned to benefit from the AI + hardware convergence, where smarter, interconnected devices become the standard in every household.

Going Global: Few Chinese tech companies are as globally exposed as Xiaomi. Roughly half of its smartphone revenue comes from overseas, with India and Europe being major markets. It’s consistently ranked among the top vendors in both regions. This global footprint diversifies its revenue base and gives it resilience against domestic volatility. And with EVs on the roadmap, Xiaomi could be looking at global automotive markets next.

New Consumption Trends: Xiaomi is at the centre of several rising trends: connected lifestyles, affordable smart gadgets, and the blending of consumer electronics with mobility. Young consumers love the ecosystem approach—buy a Xiaomi phone, and you’re more likely to buy a Xiaomi air purifier, robot vacuum, or electric scooter. It’s not just selling devices; it’s building a sticky, integrated lifestyle brand for the modern consumer.

Valuation: The stock ran up sharply in late 2024 on EV enthusiasm, and currently trades at around 44× earnings, above its 5-year average of 38×. That’s a premium valuation, especially compared to some other Prominent 10 names. Historically, Xiaomi traded much lower—around 15–20×—when phone margins were under pressure. Today’s multiple reflects growth expectations, particularly in EVs and AIoT. But to justify this premium, Xiaomi will need to keep delivering—both in product innovation and in expanding margins across its ecosystem.