The Undervalued Dividend-Paying Automotive Stock Capitalizing on EV Growth

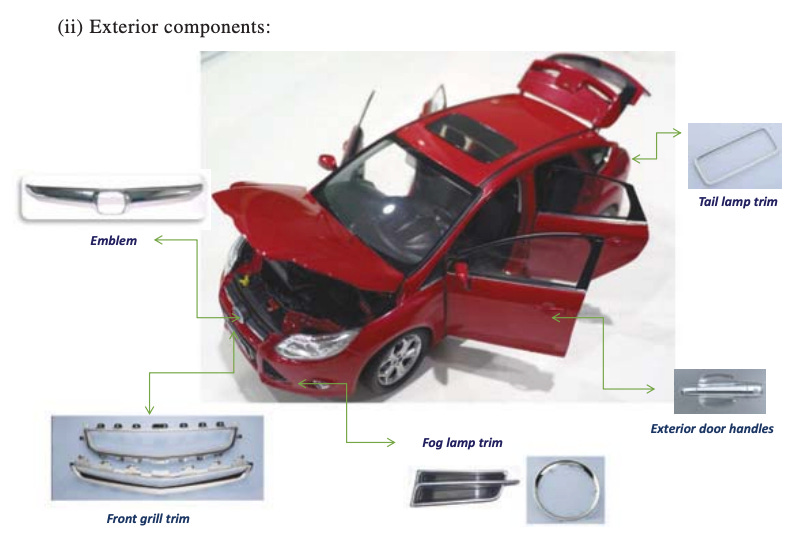

Xin Point (SEHK:1571) specializes in manufacturing electroplated components for automobiles, including decorative parts like door handles and front grills.

According to the Frost & Sullivan report, in 2016, Xin Point was the second largest automotive plastic electroplated components supplier in China in terms of revenue.

According to a report by Frost & Sullivan, Xin Point was ranked as the second-largest supplier of automotive plastic electroplated components in China by revenue in 2016. Despite this, Xin Point remains a relatively small entity with a market capitalization of HK$2.6 billion (US$333 million). For the fiscal year 2022, the company reported revenues of ¥2.883 billion (US$402 million) and net profits of ¥429 million (US$60 million).

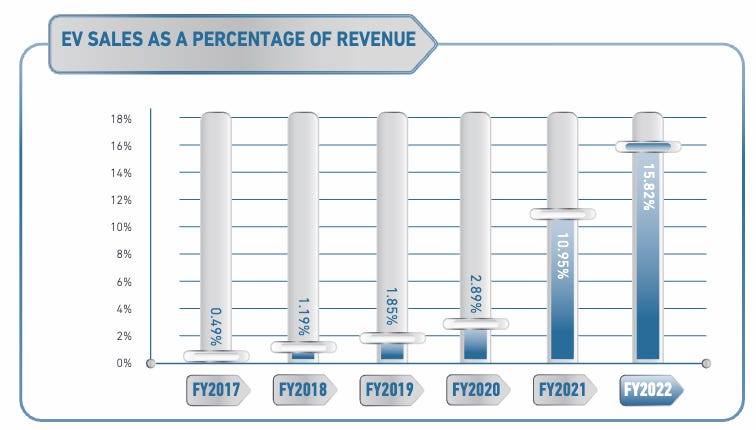

We view Xin Point as a small-cap value stock with growth potential, particularly as the automotive industry shifts from internal combustion engines to electric vehicles (EVs). This transformation is likely to spur increased demand for new EVs, which, in turn, will require electroplated parts. This trend is reflected in Xin Point's revenue growth, with a noticeable increase in contributions from EV-related sales over recent years. Given the dominance of Chinese EV brands in the market, Xin Point stands to benefit substantially from its role as a supplier to these manufacturers.